Summary: I am long the McDermott 10.625% ’24 defaulted senior notes, which trade around 12.5-13c currently. At this level I believe you are creating the recapitalized MDR equity at a low multiple of likely trough EBIT/EBITDA in FY21E – 4x EV/EBITDA, 5x EV/EBIT – with a free look at bargain basement multiples (1.5x EV/EBITDA, 1/7x EV/EBIT) if the company can execute on the mid-term financial projections it has laid before the bankruptcy court. Whilst not for the faint of heart, given the net-debt free nature of the new entity; where competing, similar EPC businesses trade; and historical M&A interest around current levels, I believe these bonds present a highly asymmetric opportunity. If MDR’s earnings power remains at historical trough levels and the new equity gets even a lowish comp multiple and/or is acquired (as was attempted in the past), you either won’t lose much or you may even earn an OK return. But if management – newly incentivized through the courts with 7.5% ownership of the pro-forma equity – can even sniff the financial targets they have laid out, then it is not hard to see bond value recover in the 40-55 range, for a potential 3-5 bagger over the next 18-24 months.

The MDR senior notes have $1.3bn face outstanding (and $1.4bn of claims per the court docket), and whilst not exactly liquid, should be tradeable for most small/mid-sized funds (as well as retail, these are tradeable on Interactive Brokers). This opportunity exists because MDR has been a dumpster fire of a situation for the better part of two years; EPC companies are complex and generally bad businesses; and this is a defaulted security, limiting interest from the market (for now).

Background:

MDR is one of the largest diversified oil & gas EPC (engineering, procurement, and construction) firms in the world, competing against the likes of TechnipFMC, Saipem, Fluor, and Subsea 7 (as well as the big boys BH, SLB, HAL, etc). The company operates globally in over 50 countries, offering services in Offshore & Subsea, Downstream, LNG, Power, Industrial Storage, and Pipe Fabrication. Through the ill-fated Chicago Bridge & Iron (CBI) acquisition consummated in mid-2018, they also acquired Lummus Technology, one of the world leaders in the licensing of IP related to hydrocarbon production across various fuels and technologies.

EPCs are lumpy, inconsistent businesses – both difficult to manage as well as value. Typically a number of companies will bid in competition for a specified project (building an LNG plant; or an offshore oil rig, etc) in a fixed price fashion, where the contractor is on the hook for any cost overruns (and similarly benefits from delivering a project below expected cost). For simple engineering jobs this is perhaps not too difficult, but for the kinds of complex, multi-billion dollar projects that global energy EPCs are attempting to deliver – often in evolving industries and emerging markets – it can lead to massive cost overruns and unexpected project losses.

The other difficulty with EPCs is the nature of cashflows associated with multi-year construction projects. MDR and its consortium may win a project to build a new LNG plant on the Gulf Coast – perhaps a $5-$10bn investment – and will be paid a small percentage of the project value when the contract is booked (and enters the backlog). However to secure the EPC’s subsequent performance on that contract, the client will require a letter of credit – partially funded at issuance by the EPC, but issued by a third party financial institution – in effect neutralizing the cash inflow impact of the contract win (or worse). Construction generally follows the percent of completion method (many of these projects are multi-year jobs), with lumpy cash flows more often weighted towards the completion of the contract – ie years after cash-out project costs have been incurred.

Thus you have this peculiar phenomenon where in periods of strong orders and growing backlogs, the cash needs of the EPC can explode, as they need to fund the LoCs to guarantee incoming orders, and may have to front much of the cash cost of construction – for years – before seeing cash inflows either at completion or as various completion milestones are reached.

Because the business is inherently cash and capital intensive; dependent upon third-party credit and financing; lumpy; and clearly hugely levered to the volatile energy industry, many of the better EPCs (Subsea 7, for example) run with net cash balance sheets and little funded debt. MDR used to be in this position, but got into huge trouble when it levered up to acquire CBI in mid-2018, both issuing a large amount of funded debt to consummate part of the purchase ($2.8bn) and inheriting CBI’s large negative working capital position – a function of CBI’s troubled legacy contract portfolio. CBI had already sold their nuclear business to Toshiba a few years ago – which operated on a similar fixed-price basis and saw similar massive overruns that bankrupted Toshiba’s subsidiary, Westinghouse, and almost the parent company as well – so it should have been apparent to MDR that the contracting culture at CBI was simply toxic company-wide. But they didn’t pay heed and closed the acquisition in April 2018.

These issues all came to a head during 2019, with MDR unable to stem the bleeding from a handful of the acquired CBI projects – principally Freeport LNG and Cameron LNG – that repeatedly experienced large cost overruns (to the tune of $1.1bn cumulative thru 2018-19) and drained cash from the now-levered MDR. To make matters worse, a stronger oil price in 2018 led to a spurt of new orders for MDR’s core onshore/offshore business – requiring the increasing posting of more and more collateral for LoCs to secure the new work entering the backlog, just as MDR’ credit quality was deteriorating. Despite a number of restructuring transactions and attempts to raise fresh capital, by mid 2019 it was clear MDR was caught in a negative liquidity spiral with no sustainable options outside of a holistic restructuring, and they filed for bankruptcy relief a few weeks ago. The first 50 pages or so of the Disclosure Statement (see here) gives a fuller account of the specifics, but at the time of the filing MDR had $4.6bn in funded debt and over $9bn in total claims (all the LoCs turned into claims upon filing).

Pro-forma Capital Structure

Thankfully, this restructuring was a pre-pack Chapter 11, with a large consensus amongst the various creditor classes, meaning it is highly likely the plan will be confirmed as is by the courts in the coming months. The key features of the restructuring are:

- Superpriority creditors ($800mm funded debt, $200mm secured LoCs pre-petition) will roll into a DIP position, injecting a further $1.2bn funded debt and $543mm further in LoC – for a total funded DIP of $2bn along with $743mm in secured LoC outstanding;

- The pre-petition revolver and term loans ($3.2bn claims) will receive $500mm in reinstated ‘take back’ secured debt, along with 94% of the new equity (subject to dilution by management’s stake and the new warrants given to the senior notes, see below);

- The senior notes ($1.3bn face, $1.4bn claim) – this is the security I own – will receive 6% in new equity (subject to dilution by the management stake, so this is really 5.5% initially), along with two tranches of warrants to purchase up to 20% total in pro-forma new equity, and the right to participate in a rights issue to raise $150mm in new equity at the Plan Equity Value;

- Management will receive 7.5% of the fully diluted newco equity;

- $276mm of vessel modification debt will be reinstated;

- All other letters of credit and bilateral facilities will be reinstated at par;

- All trade claims and executory contracts will be reinstated and honored.

During the bankruptcy proceedings, the Lummus Technology business will be sold, having already received a $2.73bn ‘stalking horse’ (minimum) bid – the proceeds of which will be used to repay the DIP and (I believe) reduce in full the secured LoCs under the DIP, with excess proceeds potentially increasing bond recovery (more below).

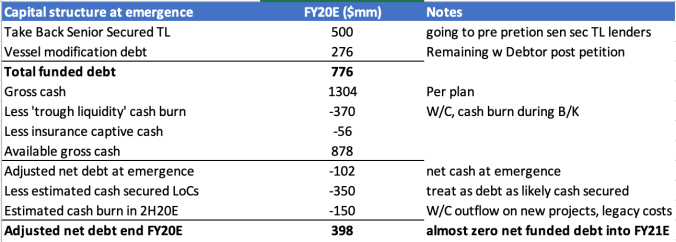

Subsequent to the Lummus sale, then, MDR will have just $776mm in funded debt (the $500mm take-back paper and the $276mm vessel modification debt), and $1.3bn of gross cash at emergence (according to the business plan and Evercore analysis included at the back of the Disclosure statement). The pro-forma capital structure – and my adjusted net debt estimate entering FY21E – is per below:

I have made a few assumptions on the conservative side in the above (more conservative, that is, than the plan analysis). Namely, I have treated $350mm of cash secured LoCs – my estimate of the minimum cash component required to secure ongoing LoCs for the business – as debt, as essentially this cash cannot be accessed by the company beyond this purpose; I have also burdened newco with assumed cash burn through B/K and in 2H20E as legacy projects complete. Nevertheless, with plan FY21E EBITDA of $640mm, the balance sheet is almost clean, with just 0.6x of adjusted net leverage based upon plan from next year.

Pro-forma Valuation

Using the estimates provided by management to the bankruptcy court, Pro-Forma valuation looks like this. Note the discrepancy between Plan Value (more expensive) and Market Value (cheaper) – since the term loans and bonds (the new equity securities) are trading ~25-30% cheap to assumed plan equity value. Also, I leave FY20 out of it since half the year will be consumed by the court process, and I have already taxed newco EV with the estimated losses/cash burn from 2H20E, so I think its right to appraise the new MDR based on 2021 numbers and onwards:

Hence newco is on around 4x FY1 EV/EBITDA, and 1.5x FY2 EV/EBITDA…if they can hit management projections. Clearly the market is implying they won’t even get close.

Perspectives on Newco Earnings Power

The market is right to be skeptical given MDR’s recent history: ever since acquiring CBI, MDR has reported disappointment after disappointment as project costs just kept spiraling. In early 2019 MDR guided to FY19 EBITDA coming in north of $1bn; in reality the number will probably be in the $300-400mm range, with a similar massive shortfall on cashflow. Certainly, the CBI acquisition was an unmitigated disaster.

But there are reasons to believe there is a path forward, and that basically all the recent margin contraction lies squarely at the foot of a few bad CBI contracts. Management’s estimates suggest EBITDA of $640mm in FY21E and >$1bn in FY22E, implying EBITDA margins of 6%/8% on the record backlog currently north of $20bn. Whilst certainly higher than the horrific 2018/2019 performance, this is not materially different from MDR’s recent earnings power, and is much lower than the kinds of margins MDR used to earn on a much smaller book of business. For example, in the 2006-12 period, MDR averaged 12% EBITDA margins – admittedly this came during a much higher and prosperous oil price environment. They then had another kitchen-sink year in 2013 which prompted the hiring of David Dickson (who had previously fixed Technip), but in the 2014-2017 period, they still managed 8.5% average EBITDA margins – clearly far lower than during the previous cycle but not materially different from current implied guidance. Note also that this was for the pre-CBI business and excluding Lummus (the much higher margin technology licensing business), when the revenue scale of the business was less than half the expanded footprint now, so I don’t think it is an unrealistic target for the go-forward business, ex the problematic CBI projects.

This hypothesis appears at least partially supported by the earnings trajectory since the CBI deal closed. In 1Q 2018 – before CBI closed – MDR standalone reported 17% EBITDA margins. In the period 2Q’18 thru 3Q’19, EBITDA margins have dropped to 4.2% as a result of ongoing CBI project losses. But if we strip out the discrete CBI projects from EBITDA (along with attendant revenues), ‘core MDR’ EBITDA margins amounted to 7.7%. And if we remove Lummus Tech earnings and revenues (since this business will be sold), remainco MDR margins remain reasonable at 6.2% – still low by historical standards but above the FY21E estimates provided in the new business plan.

But I believe we need to stretch slightly further than this, understanding that most of this core MDR earnings deterioration occurred in 2Q’19 (2.1% reported EBITDA margins ex CBI) and 3Q’19 (5.2% reported EBITDA margins ex CBI) – when it was already abundantly clear that MDR would need to be restructured in the courts. Management has a huge amount of discretion in when to book losses on troublesome contracts and, heading into an imminent Chapter 11, where management was already in line to receive some back-end equity in the new company, it’s entirely believable they started kitchen-sinking costs on other projects (in particular, there was a $256mm provision in the most recent quarter that appears to cover a number of non-CBI contracts just before the B/K filing).

A final reason to affirm the believability of the new forecasts is that the legacy CBI exposure is now de minimis. The vast majority of losses occurred on two projects – Cameron LNG, and Freeport LNG – which are now either complete or will be by the time MDR exists the court-led process (by mid-year). Meanwhile, the legacy CBI contracts remaining within MDR’s backlog are only $1.5bn (out of total backlog >$20bn), of which only $0.4bn will be left by 2020 year-end. It stands to reason, then, that the worst re CBI has passed.

Suffice to say, while it is extremely difficult to benchmark the true earnings power of core MDR post restructuring, I am reasonably confident the numbers can’t get much worse; that 6% newco MDR EBITDA margins are eminently sustainable as a low-end case; and that high single digit EBITDA margins on the go-forward book of business don’t look outrageous at all.

Where should this trade?

Whilst delevered, MDR will not generate any FCF in FY21E so this is, unfortunately, a multiples-based comparison (even though I think it will generate substantial FCF thereafter). However, I am less loathe to this relative value approach than normal, because there are a number of clear comps for MDR (who suffer from the same business model flaws and yet trade in the market where they do); and also because I believe there is a decent chance MDR is acquired, in whole or in part, at levels that underwrite a multiples-based valuation even in the absence of immediate cash flow.

We can debate business quality and how much to tax MDR for going bankrupt; but most all the other EPC contractors, even in a down market, trade in the 4-6x EV/EBITDA range (or higher, for the higher quality names like HAL, BH, SLB, etc) and high single digit multiples of EBIT. Here is the implied equity value for newco MDR, and the implied bond recovery SOLELY ON THE INITIAL 5.5% fully diluted equity stake, based on a range of EBITDA and multiple scenarios:

Ref a current bond px of ~12.5c, it seems MDR newco equity would have to trade at the very low end, or below, sector comps, and never recover beyond $650mm in EBITDA, for you to lose much value here; meanwhile if management gets close to its EBITDA projections and this trades at a sector multiple the bonds are a double or thereabouts.

But this is only part of the equation, since bondholders also receive two tranches of warrants:

- The right to buy 10% of the fully diluted equity for 7 years, at a strike equal to ~130% of equity plan value (ie, I think $3.1bn equity vs plan value $2.35bn)

- The right to buy 10% of the fully diluted equity for 7yrs, at a strike equal to ~170% of equity plan value (thus $4bn vs plan value $2.35bn)

A simple Black-Scholes model with conservative assumptions (40% IV, 3% interest rates) suggests huge value to these warrants: around 39% of notional for the first tranche, and 21% of notional for the second tranche (and thus, 3.9% of newco equity for tranche 1 and 2.1% of newco equity for tranche 2, since each tranche is for 10% of newco equity).

Since, however, the warrants still require bondholders to tip in new money (if the equity rises above strike), I have decided to value the warrants at intrinsic value, across the various scenarios outlined above, in determining how much upside bondholders today may receive. Whilst conservative, this assumes bondholders don’t want to put more money into MDR even if it rallies, and would be more likely to sell their equity optionality at or near intrinsic value if such a situation arises in the coming years.

Doing this – and diluting down the original 5.5% equity ownership for each of the new warrant tranches, assuming they are in the money – and total bondholder recovery at these EBITDA and multiple assumptions looks like this:

This is how – in a scenario where management simply hits their business plan and the stock gets a peer multiple – bondholders could see up to a 4-5x return, I think in <2 yrs.

Other considerations

There are a few other factors to consider which I believe could add to further upside optionality in the situation:

Lummus Technology sale: this is a crown jewel business, reporting 30% operating margins and 40%+ ROICs with secular growth despite cyclicality in the underlying commodities; the stalking horse bid is around 12-13x free cash flow, which seems low for a business of this quality. During the bidding process, there were 18 bidders, with 5 offering to become the stalking horse. There may well be some anti-trust risk with some of these bidders (given concentration in the market), but there is a reasonable chance there is an overbid during the court-led auction, in which case the bonds would likely end up with a higher than 6% stake in new MDR equity (the math is quite complicated, excess value follows a paydown waterfall with bondholders last in line). It is hard to parse out but I think a 10% increase in the bid price could increase bondholder equity by at least a couple of percentage points – clearly very meaningful given my forward view on the business and the current bond price.

M&A takeout risk: In early 2018, Subsea 7 tried to buy out MDR for $2.1bn EV; MDR decided to go ahead with the CBI merger instead (oops). Still, at the time, Subsea was willing to pay 5x LTM EV/EBITDA and 7x LTM EV/EBIT, for a business that was admittedly more profitable but also far less diversified and had just a $4bn backlog (versus $20bn today, $19bn of which is non-legacy CBI). Since the plan enterprise value today is around $2bn – excluding Lummus of course – and comes with the much higher backlog and (theoretically) the greater scale and cost synergies of the CBI transaction, but without all the legacy costs, I don’t see why a bid today for new MDR should be much lower than this – in fact it could be a good deal higher. But in any case, either in absolute terms – $2.1bn – or in multiples terms – 5x EV/EBITDA – a potential Subsea bid again implies little to no downside for the bonds from here (11c), even on trough EBITDA ($650mm), and even assuming no value given for the warrants (highly unlikely in my view).. Of course there are also other likely bidders – not least the new TechnipFMC spinco (separating in 2H this year), which will focus on global energy EPC with a large position in LNG and smaller positions in other segments – largely complementing MDR’s go-forward positions. It would not be a surprise, then, to see bids either in whole or in part for newco, probably post-emergency once it is fully cleansed of the CBI stink. And since the term lenders will own the majority of newco equity and want their money back (they receive 84c in the dollar according to plan value, implying they need a ~30% premium to plan to get their money back), I believe any acquisition would have to be at a meaningful premium to plan value at the very least.

Risks

No investment without risk and bankruptcy securities have plenty of them. Beyond the obvious, though (plan not being confirmed; further deterioration in legacy projects; etc), the biggest risk is clearly energy markets fully rolling over. MDR has accumulated a significant backlog during lumpy periods and a time of gargantuan internal distress, but I would imagine if oil remarks to $40/bbl a good portion of the backlog may drop out. This will clearly affect plan values and ultimate recovery as absolute EBITDA will necessarily fall. There is no way around this risk other than to hedge for a lower oil price environment – something I do not really portend, but its an inherent risk to the thesis.

Disclosure: Long MDR 10.625 ’24 defaulted bonds

If the bonds trade for 12.5c and the total bondholder claims are $1.4b and the bonds get 5.5 percent of the equity, then my math is:

$1.4b x .125 = $175 million market value of bond claims.

$175m/0.055 = $3.18b implied equity value.

I get that some of the bond value may be attributable to the warrants and therefore lower the implied equity value. But this is quite off from the plan Enterprise value of $2b. What am I missing?

Thanks and good article.

hi there. yes you can’t straight extrapolate from just the 5.5% to work out the implied equity value given the huge value of the warrants as part of bondholder recovery (your math essentially implies that the $1.4bn bondholder claim stops with just 5.5% of equity, which is not true). instead i extrapolate the current market implied equity value from the term loans – which are entirely recovering equity, no warrants – so its a clean comparison. this is how i get my ‘market implied value’ which is considerably less than ‘plan value.’

great write up. lots of smart guys in both the bonds & the TL. can you explain how you value the warrants & rights? struggling w/ math a bit similar to prior question. thx much

the math is a bit complex. i don’t value the rights at all – since the bonds/TL currently trade well below plan value and the rights only give you the right to acquire more shares at plan value (clearly no one is doing that unless the TL trades thru 84 and the bonds trade closer to 20). so you can forget about that part of it.

the warrants are not difficult to value – you just need to work out what the ‘strike’ is (in terms of equity value) – then use a Black Scholes calculator (you can find these on the net) and put in the relevant inputs (7yr maturity, strikes, implied vol assumption, interest rate assumption, etc). you can fairly easily work out the theoretical value of the warrants under given assumptions. as you would expect, a 7yr option on 10% of the pro-forma equity for a very volatile stock/company is likely to be worth a significant amount of that 10% stake – and indeed that’s what black scholes suggests (i think tranche one is worth ~3-4% of newco equity value and tranche two is worth 2-3% of newco equity value – hence adjusted equity ownership on the bonds is closer to 10-11% of newco pro-forma than the stated 6% pre dilution).

Pingback: McDermott Defaulted Debt: A Compelling Speculation - McDermott International, Inc. (OTCMKTS:MDRIQ) - Supply Chain Council of European Union | Scceu.org

Hello,

New to investing. I’ve had 18,216 shares at $1.51 since August 2019. My current thought is to sell these shares at the first spike of volatility that I see on the OTC market. My question: given all of your speculative scenarios above. Is it wise to hold my shares until the end of bankruptcy? Any input is appreciated. Thanks!

hi Casey – I’m sorry to say your shares will be canceled as per the bankruptcy plan, and are therefore worthless. you should probably sell them as soon as possible to recover whatever residual value you can.

Jeremy, I’ve always enjoyed your posts. Thanks for doing them. Do you have a fund or SMA for outside investors? Thanks Brian

Sent from Yahoo Mail for iPhone

hi Brian – many thanks for your interest. please email me at jeremy.raper@gmail.com to discuss further. thank you.

Hi Jeremy,

Thanks for maintaining this blog — you do great work and I look forward to every new post.

A bit off-topic, but I was curious whether you have any thoughts on Showa Denko (4004 JP) or Tokai Carbon? In the case of the former, they’ll have substantial leverage following the acquisition of Hitachi Chemicals and their key end market (graphite electrodes) appears to be under pressure.

hi there – thanks for the kind words! I am very familiar with both those companies, and don’t disagree – although it is also quite cheap on a headline level. It is probably worth doing more work on given the HC acquisition, i just haven’t had time to run the rule over that deal yet…